by Chris Nicholson | Jan 3, 2019 | Blog, Group Insurance

Sales goals, service goals, project goals and so many more goals that businesses often create this time of year. Are we doing better than last year? We’ve been part of many conversations with our clients about their goals for their business. We love talking to...

by Chris Nicholson | Nov 26, 2018 | Dental

Warning – Your next dentist visit could cost you more than you think! Your dentist is trying to provide you the best service they can, but where the world of dental expertise and insurance coverage intersect is a dangerous one that can leave you with a bill for...

by Chris Nicholson | Oct 19, 2018 | Blog, EAP, Small Business

It can be difficult to separate personal challenges from your day-to-day work life. The Arive® Employee Assistance Program – included in some benefits packages – gives you access to qualified professionals who can help you handle situations impacting your emotional...

by Chris Nicholson | Jan 5, 2018 | Blog, Group Insurance

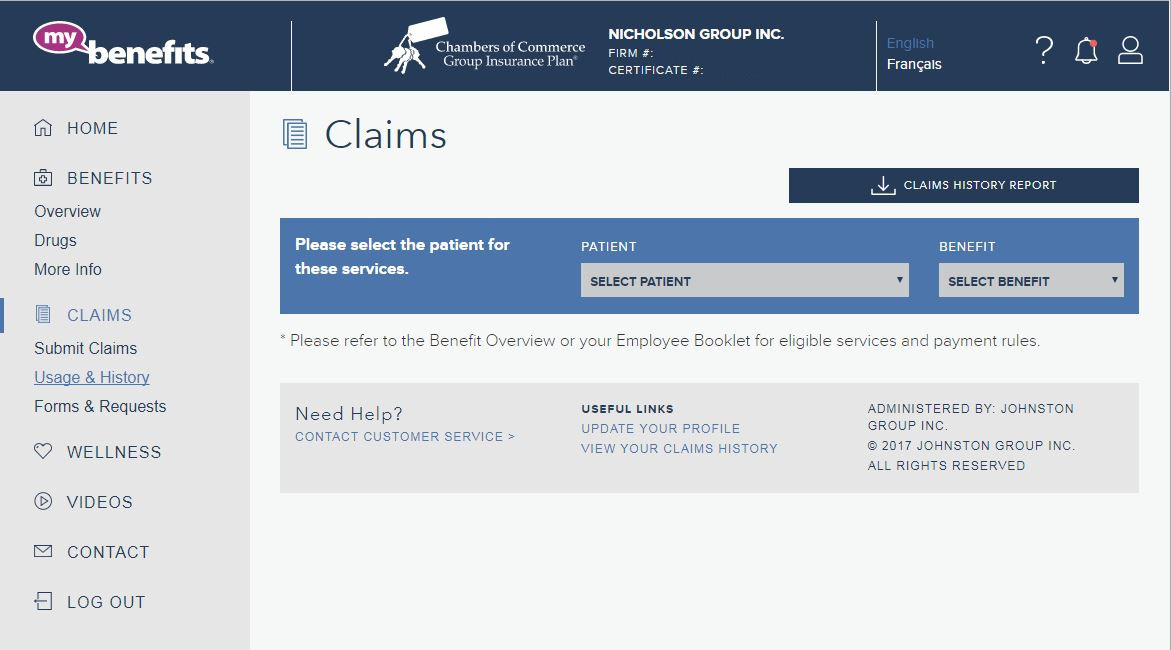

If you are looking to get your claims report for 2017 to use for your personal or business income tax purposes. Log into my-benefits.ca CLICK HERE Click on Usage & History Click on the Claims History Report button. Select January 2017 – December 2017 Print...

by Chris Nicholson | Dec 1, 2017 | Blog, Drugs, Group Insurance

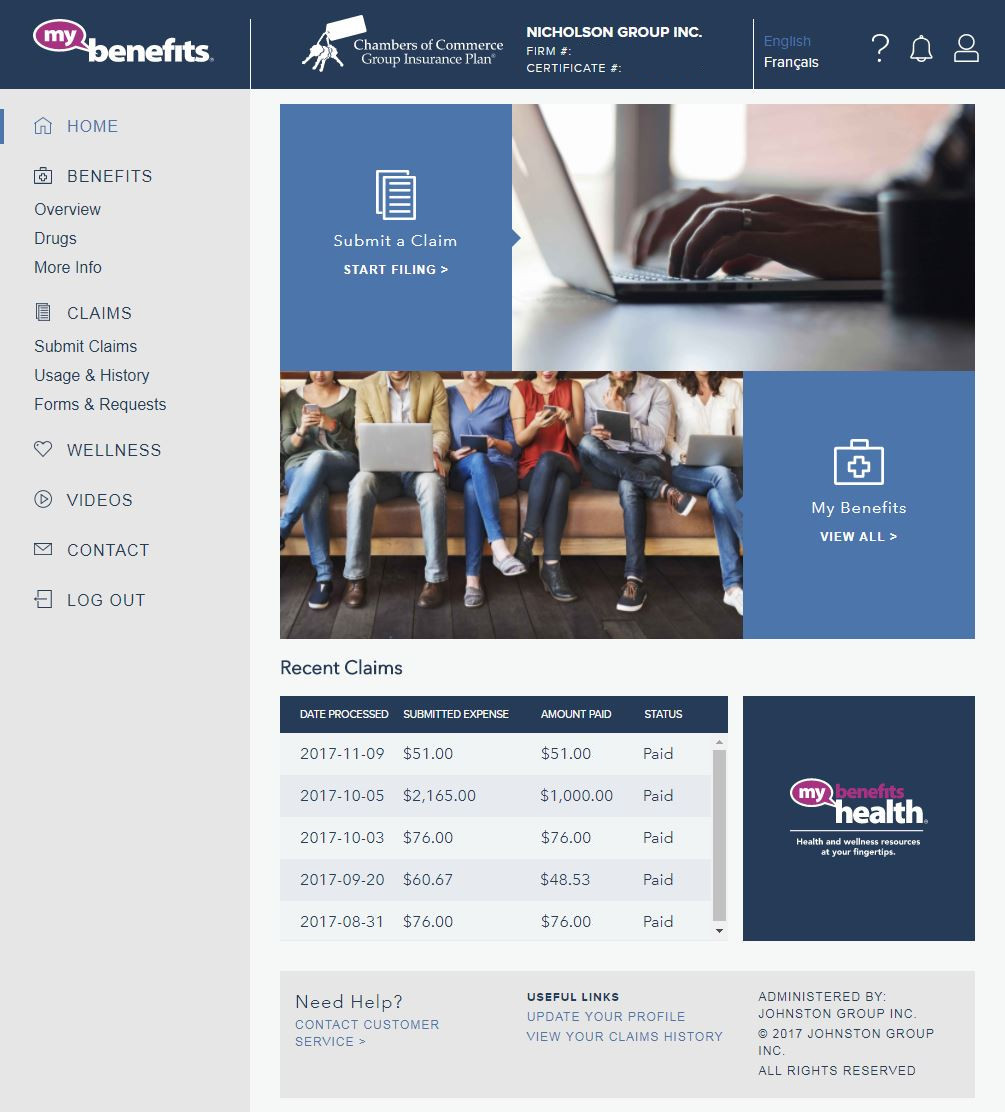

For Members of the Chamber Plan, Maximum Benefits or Johnston Group’s ContinYou or Retiree Plans the My-Benefits.ca website has had a fresh new update! It’s a high quality responsive design that works well on computer, tablets and phones, (There’s an...

by Chris Nicholson | Nov 2, 2017 | Blog, Group Insurance

Derek Nicholson is a firm believer in the value of insurance and loves working with his wife and son to offer the Chamber of Commerce Group Insurance Plan to chamber members and their employees. He knows better than most how quickly life can change. On October 29,...